The Use of Testamentary Charitable Lead Annuity Trusts (TCLATs)in Estate Planning

With the Trump tax cuts set to expire on December 31, 2025, many wealthy individuals and families are searching for additional tools to help them pass large amounts of wealth to lower generations to avoid the imposition of the federal estate tax. In many instances, the use of credit shelter trusts, SLATs, and the portability election are simply not enough to shelter a family’s wealth from the assessment of the death tax. In those instances, consideration may be given to the use of a Testamentary Charitable Lead Annuity Trust, which can serve a dual purpose – assisting a favorite charity while providing for a future bequest to lower generations.

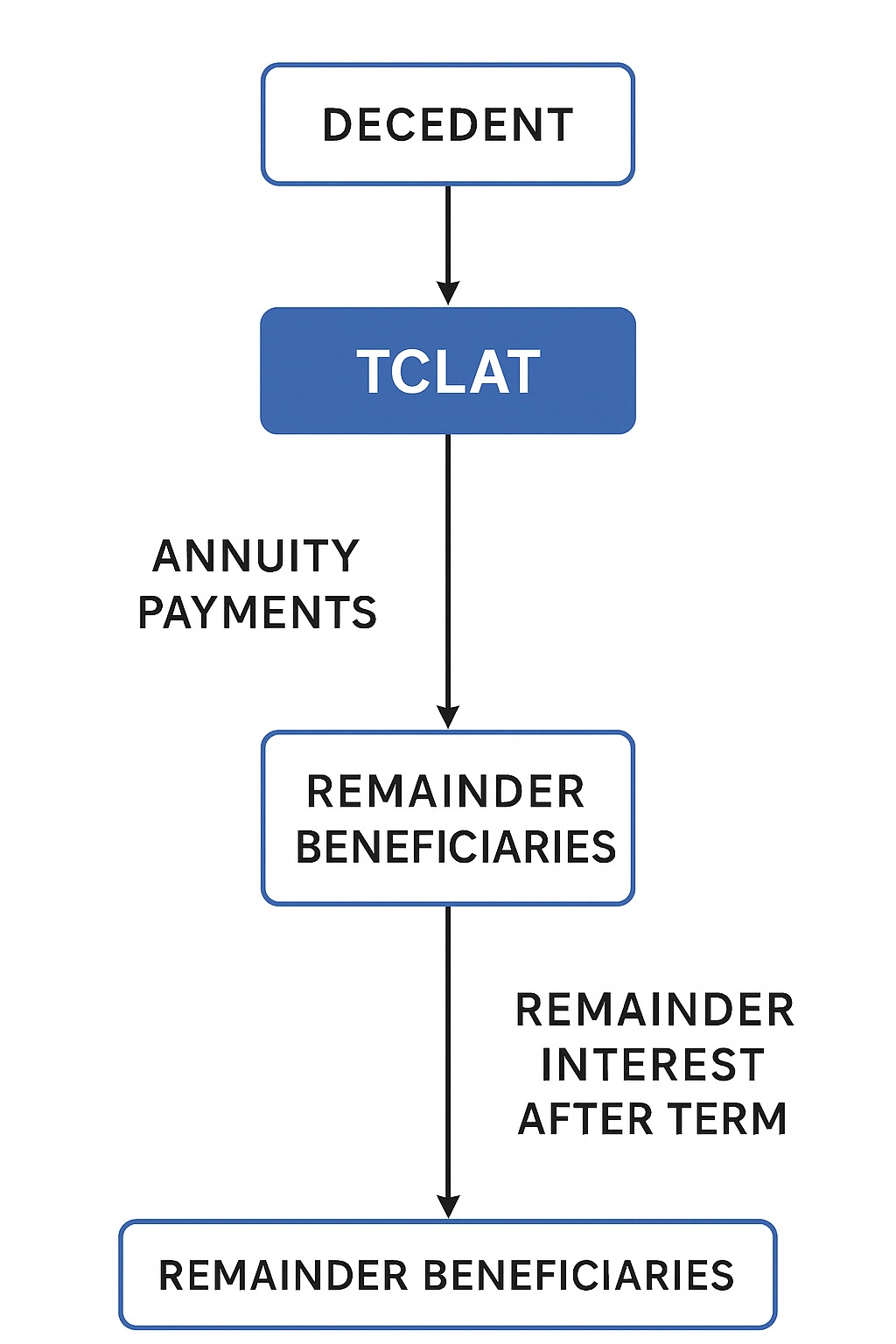

The Testamentary Charitable Lead Annuity Trust (TCLAT) is a powerful estate planning vehicle that combines philanthropic intent with tax-efficient wealth transfer. A TCLAT allows a decedent’s estate to provide a stream of income to one or more charitable beneficiaries for a fixed term of years or for the life of an individual, with the remainder passing to non-charitable beneficiaries such as family members. This structure provides a charitable estate tax deduction at death and can result in significant wealth transfer with reduced or eliminated transfer tax liability.

What Is a Testamentary Charitable Lead Annuity Trust (TCLAT)?

A TCLAT is a type of charitable lead trust (CLT) created upon the death of a decedent under the terms of a will or revocable trust. It is structured to provide a fixed annuity payment to a qualified charitable organization for a specified term of years or for the life of an individual. After the term ends, the remaining trust assets pass to non-charitable remainder beneficiaries, often the decedent’s children or other heirs.

Unlike inter vivos CLATs, a testamentary CLAT is funded at death, and the estate receives a charitable estate tax deduction for the present value of the annuity payments to be made to charity.

Legal authority:

IRC § 2055(e)(2)(B): governs split-interest charitable gifts and sets the requirements for a deductible charitable lead interest.

Treasury Regulation § 20.2055-2(e)(2)(vi): provides the requirements for fixed annuity payments.

IRC § 7520: governs the actuarial assumptions used to calculate present value.

Revenue Ruling 88-27, 1988-1 C.B. 331: affirms that a charitable lead annuity trust may qualify for the estate tax deduction if properly structured.

Characteristics of a TCLAT

The general characteristics of a TCLAT are as follows:

They are created by a will or revocable trust and takes effect at death.

It pays a fixed annuity (a sum certain) to one or more qualified charitable organizations under IRC § 170(c).

The trust’s remainder passes to individuals or trusts after the annuity term expires.

The trust must meet qualified interest rules under IRC § 2055(e)(2)(B).

The trust must be irrevocable upon creation.

Suitable Clients for a TCLAT

A TCLAT is most suitable for high-net-worth individuals who:

Have philanthropic goals and wish to benefit charities posthumously.

Anticipate a taxable estate, especially with the looming sunset of the Tax Cuts and Jobs Act (TCJA) in 2026, which may lower the federal estate tax exemption from $13.99 million (2025) to approximately $6.8 million (adjusted for inflation).

Want to provide for heirs at a reduced estate tax cost, particularly when market growth is expected to exceed the IRC § 7520 rate.

Do not require income from the assets during life, making the TCLAT a better fit for testamentary use rather than lifetime planning.

Calculating the Charitable Deduction

The grantor’s estate receives a charitable deduction under IRC § 2055(a) for the present value of the charitable annuity stream.

The deduction is calculated using:

The annuity amount (a fixed dollar sum).

The term of years (or life expectancy of a measuring life).

The IRC § 7520 rate (published monthly by the IRS).

The fair market value of the assets used to fund the TCLAT

For Example:

Estate funds TCLAT with $5 million.

Annuity of $300,000 per year for 20 years to a public charity.

§ 7520 rate is 5.2% (April 2025).

Using actuarial tables (IRS Publication 1457), the present value of the annuity is approximately $3.8 million.

The estate receives a charitable estate tax deduction of $3.8 million, reducing the taxable estate accordingly.

Important Note: If the present value of the annuity stream equals 100% of the funding amount, this is called a zeroed-out CLAT, which can pass remainder assets to heirs free of estate tax if growth exceeds the § 7520 rate.

Benefits to the Charitable Beneficiary

The charity receives predictable and reliable payments each year, facilitating long-term planning.

Payments are not contingent on the trust’s investment performance, unlike a charitable lead unitrust (CLUT).

The trust is generally structured to pay the annuity annually, although more frequent payments are permitted.

Charities can use these annuities to fund endowments, capital campaigns, or ongoing operations.

Timing of Remaindermen’s Inheritance

The remainder beneficiaries do not receive distributions until the end of the annuity term.

This period can range from a fixed number of years (e.g., 10–30 years) to the life expectancy of a named individual (e.g., the decedent’s spouse).

The longer the annuity term, the greater the charitable deduction, but the longer the wait for non-charitable beneficiaries.

Taxation and Reporting Requirements

The trust is a complex trust under Subchapter J and must file IRS Form 1041 annually.

The trust is generally not a grantor trust, so it pays its own income tax, but deductions are allowed for annuity payments to charity under IRC § 642(c).

Any income earned and not used for charitable payments may be subject to trust tax brackets, which are highly compressed.

Practical Example

Facts:

Jane, a widow, has an estate of $20 million.

She includes in her will a provision to fund a TCLAT with $5 million.

The trust will pay $250,000 annually to the Red Cross for 20 years.

The remainder goes to her three grandchildren.

Result:

The charitable deduction is approximately $3.9 million based on § 7520 rate of 5.2%.

Estate tax is reduced due to the deduction.

If trust assets grow at 8% annually, the remainder passing to the grandchildren could exceed $2.5 million estate-tax free.

Conclusion

The Testamentary Charitable Lead Annuity Trust offers a compelling strategy for high-net-worth individuals to reduce estate tax liability while making a lasting philanthropic impact. The ability to generate a sizable charitable deduction, lock in benefits for a preferred charity, and transfer appreciating assets to heirs with minimal transfer tax makes the TCLAT a strategic tool in post-mortem estate planning.

However, due to the technical requirements of IRC § 2055 and the valuation rules under § 7520, the trust must be carefully drafted to ensure qualification for the charitable deduction. With proper implementation, the TCLAT can serve as a legacy-enhancing structure that meets both charitable and familial objectives.